Accidental Damage Insurance

What is accidental damage insurance?

Accidental damage is an optional cover extension, which can be added to both buildings and contents cover when you purchase a Homeprotect policy.

We define ‘accidental damage’ as a sudden, unexpected, and unforeseen event that results in physical damage and has been caused by a policyholder, an occupant of the property, an invited guest, domestic staff (e.g. a cleaner), a third party (e.g. a delivery person) or a wild animal (e.g. a fox).

Accidental damage for buildings

We offer two levels of accidental damage cover for buildings – Basic Accidental Damage and Full Accidental Damage.

Basic Accidental Damage

Our Basic Accidental Damage cover provides up to £1,500 of cover (per claim) for accidental damage to:

- fixed glass in windows, doors, fanlights, skylights

- solar panels

- fixed sanitaryware and bathroom fixtures

- ceramic or induction hobs

Cover is provided in the main home only, not in outbuildings.

Full Accidental Damage

Full Accidental Damage extends cover to all parts of your home and outbuildings. So, for example, if you have a DIY disaster and damage the structure of your home, you’ll be covered.

Your main building will be covered up to your buildings sum insured per claim (typically £1 million) and your outbuildings will be covered up to your outbuildings sum insured per claim (typically £20,000 unless you have requested more). The exception to this is in the event of damage to carpets, where there is a £750 claims limit.

Damage to Underground Services

Under both our Basic and Full accidental damage options, we also cover damage to underground services (no matter whether the damage was caused accidentally or not).

We define underground services as cables, drain inspection covers and underground drains, pipes or tanks providing services and for which you are responsible.

The cover includes tracing, accessing, and repairing the source of the damage to the underground services as well as reinstating any wall, floor, ceiling, drive, fence or path removed or damaged during the search – but only within the claim limit.

In the event of a blockage of an underground pipe or drain, cover is provided to trace, access and clear the blockage on the basis that you have tried, unsuccessfully, to clear it first using established methods such as rodding.

There are cover restrictions which you should be aware of:

Restrictions for Basic cover only

- there is a claim limit of £1,500 on any claim involving underground services

- damage to septic tanks, cesspits, or sewage treatment centres

Restrictions for Full cover only

- any amount over £5,000 per claim involving blockage of an underground pipe or drain

Restrictions for both Basic and Full cover

- damage to pitch fibre drains caused by inherent defects in the design, material, construction or installation of the pipes and drains

ACCIDENTAL DAMAGE: Compare Basic and Full cover levels

| BASIC | FULL | |

|---|---|---|

| Limit per claim (your home) | £1,500 | Buildings sum insured |

| Fixed glass in windows, doors, fanlights, skylight | ✖ | Outbuildings sum insured |

| Fixed sanitaryware and bathroom fixtures | ✔ | ✔ |

| Ceramic or induction hobs | ✔ | ✔ |

| Solar panels | ✔ | ✔ |

| Damage to underground service pipes or cables | ✔ | ✔ |

| Blockage of underground pipes or drain | ✖ | £5,000 / claim |

| Other incidents (e.g. damage to roof, walls, floors, doors, fixtures & fittings) | ✖ | ✔ |

| Permanent outdoor structures (e.g. boundary walls) | ✖ | ✔ |

| Fitted carpets | ✖ | £750 / claim |

| Damage caused by vermin (e.g. rats, mice) | ✖ | ✖ |

Get a home insurance quote online

Get a quote online in less than 10 minutes*

Accidental damage for Contents

We offer two levels of accidental damage cover for contents – Basic Accidental Damage and Full Accidental Damage.

Basic Accidental Damage

Our Basic Accidental Damage cover provides up to £1,500 of cover (per claim) for accidental damage to non-portable consumer electronics used for entertainment purposes, such as:

- desktop computers and monitors

- DVD and Blu-Ray players

- gaming consoles

- home cinema system

- sound systems

- TVs

There are a number of restrictions and exclusions which could prevent an accidental damage claim from being successful:

Restrictions for Basic cover only

- damage to portable electronic gadgets (e.g. laptops, mobiles, iPads etc)

- any amount over £1,500 per claim for damage inside the home

- any amount over £1,000 per claim for damage outside the home (e.g. in the garden)

Restrictions for Full cover only

- any amount over £750 per claim for damage to carpets

- any amount over £1,000 per claim for damage to brittle items (e.g. glass or china)

- damage to money, documents, or stamps

- damage to any of the following items, with a replacement value of £1,500 or more, as these are Specified Items:

- High Risk Items (either individually or as part of a collection)

- Electronic Gadgets (including mobile phones)

- Bikes

Restrictions for both Basic and Full cover

The following restrictions and exclusions apply:

- damage caused by overflowing water (e.g. where a bath has been running and left unattended)

- breakdowns, mechanical faults, or electrical faults

- gradual damage or damage caused by neglect, lack of maintenance, poor design or poor quality installation

- pet damage

- damage caused by contractors

- deliberate or reckless damage

- accidental loss

ACCIDENTAL DAMAGE TO CONTENTS: Compare Basic and Full cover levels

| BASIC | FULL | |

|---|---|---|

| Limit per claim | £1,500 | Contents sum insured |

| Non-portable electronic devices used for entertainment (e.g. TVs) | ✔ | ✔ |

| Portable electronic gadgets (e.g. mobiles, laptops) worth less than £1,500 individually | ✔ | ✔ |

| Household appliances | ✖ | ✔ |

| Household items | ✖ | ✔ |

| High Risk Items (worth less than £1,500 individually) | ✖ | ✔ |

| Furniture | ✖ | ✔ |

| Business equipment (owned by you) | ✖ | £3,000 / claim |

| Visitor contents | ✖ | £2,500 / claim |

| Rugs and carpets | ✖ | £750 / claim |

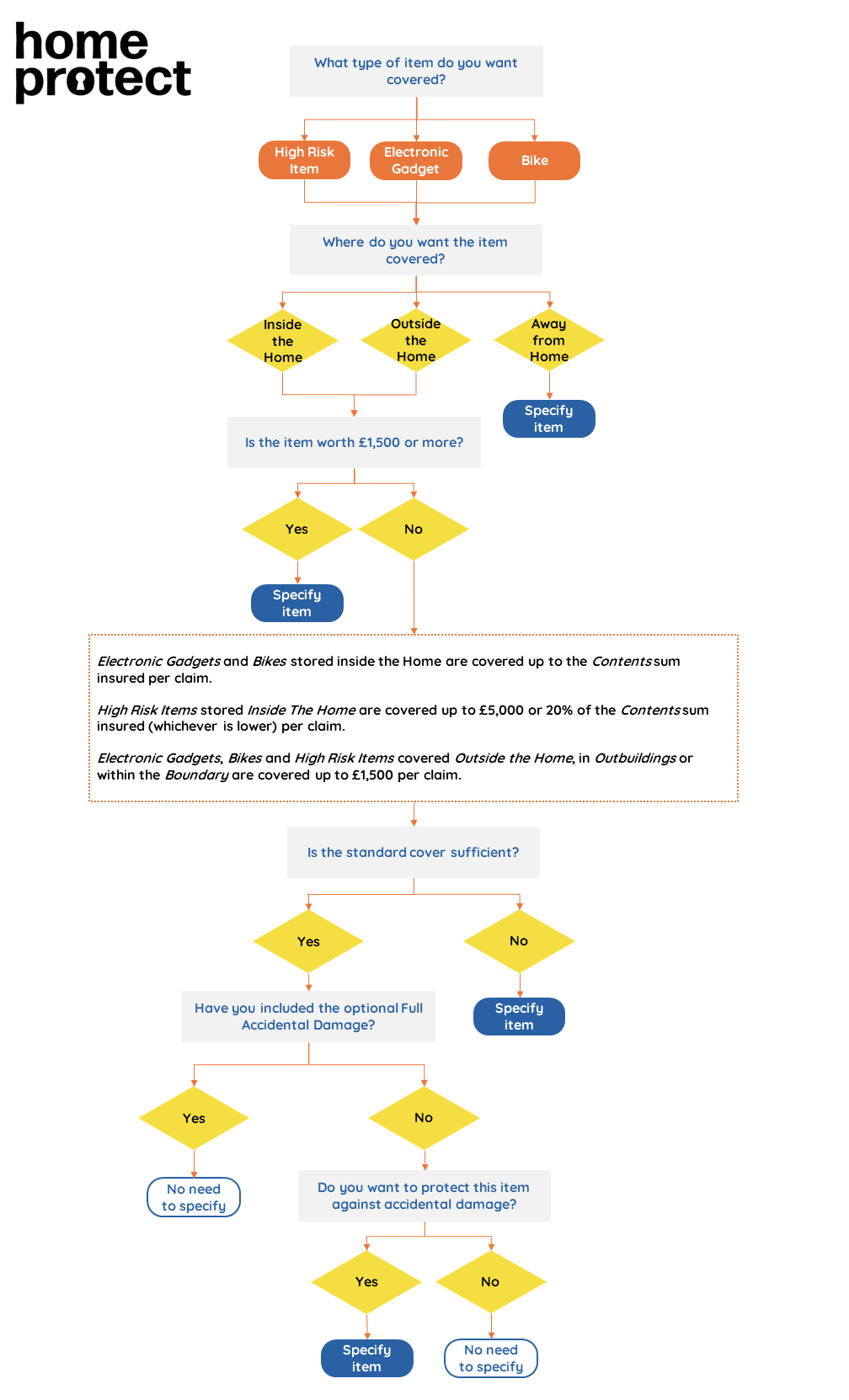

Accidental damage to electronic gadgets, bikes and high risk items

If you have Full Contents Accidental Damage, then you are covered inside the home for:

- Bikes (including electrically assisted pedal bikes) individually worth less than £1,500

- Portable electronic gadgets (e.g. laptops, mobiles, iPads, Airpods etc) individually worth less than £1,500

- High Risk Items individually (or as part of a collection) worth less than £1,500 (but only up to £5,000 in aggregate)

For reference, High Risk Items are defined as any of the following:

- clocks

- coin collections

- furs

- gold, silver and other precious metals (including plated items)

- guns

- jewellery and watches

- medals

- medical equipment (including hearing aids)

- ride on or robotic lawnmowers

- stamp collections

- wheelchairs or mobility scooters

- works of art

If you have bikes or electronic gadgets individually worth £1,500 or more, or you want cover away from the home, then you can specify these on your policy (specified items are covered for physical damage and theft).

If you store your bikes in an outbuilding (e.g. a garden shed) then consider that there is a claim limit of £1,500 for items stored in outbuildings. You have a couple of options here. You can either call us and our underwriters can potentially increase the outbuildings limit. Alternatively, you can specify your bikes on your policy (specified items are covered for physical damage and theft). For example, if you have three bikes, each worth £1,000 each that you store in your garden shed, you may choose to specify them to ensure the full replacement value of all three bikes is covered.

If you have High Risk Items individually worth £1,500 or more, or you need more than the £5,000 aggregate limit, then you have a couple of options. You can either call us and our underwriters can potentially increase both the individual item limit and the overall aggregate limit. Alternatively, you can specify your items on your policy (specified items are covered for physical damage and theft). For example, if you have 10 pieces of jewellery, each item worth £1,000, you may choose to specify them to ensure the full replacement value of all 10 pieces is covered.

Have a look at this flow chart diagram to help you decide whether to specify High Risk Items, electronic gadgets and bikes.

{kind=link}

Accidental damage to Personal Possessions

We define personal possessions to be items likely to be worn, carried, or used by you away from the boundary of your property, such as bags, clothes and sports equipment.

If you are concerned about accidental damage to personal possessions, then you can purchase this cover option (which is separate to accidental damage to contents).

Accidental damage to matching items and sets

We treat any individual items of a matching set or suite of furniture, sanitary ware, or other bathroom fittings as a single item. We will pay you for individual damaged items (subject to any claim limits) but not for undamaged companion pieces.

If the individual damaged items cannot be repaired or a replacement found we will also pay up to 50% towards the undamaged part of the set or suite of furniture, sanitary ware or bathroom fittings.

If a floor covering is damaged beyond repair, we will only pay to have the damaged floor covering replaced. We will not pay for undamaged floor covering in adjoining rooms.

Your Questions Answered

Accidental damage cover does not have a fixed price. Rather we calculate the cost of accidental damage cover based on the value of the buildings and/or contents, together with the perceived risk we take on as an insurer for provision of accidental damage cover. This varies from person to person.

Accidental loss is the loss of any item of your contents, inside or away from the home. Accidental loss is not covered by a Homeprotect policy.

Accidental damage is the most common type of claim we receive for buildings and contents (closely followed by escape of water).

A house fire may be caused on accident, but we would classify it as fire damage. So it wouldn’t matter if you did not have accidental damage cover, we would cover a fire under the fire event.

No accidental damage does not cover wear and tear.Wear and tear is a standard exclusion in home insurance policies.

Landlords who opt for both our buildings and contents cover (if they are providing a furnished property) can claim for accidental damage if a tenant causes accidental damage to the landlord’s property.

Tenants would need their own contents insurance policy – including accidental damage cover – to be able to claim for accidental damage to their own possessions.

The answer to this question very much depends on your risk tolerance. Are you the sort of person who is very careful when it comes to your home and possessions? If so, you may find the chances of you needing accidental damage are slim, therefore it may not be worth the additional cost.

Specifically in terms of contents insurance, you should consider whether it’s worth paying for accidental damage cover (either basic or full cover) if in reality you’re only concerned about one or two valuable items (e.g. an expensive laptop). In which case you should consider whether it’s more appropriate to specify these items (which provide cover against theft and physical damage), rather than buy accidental damage cover.

Another consideration is your excess. You will have a compulsory excess for both buildings and contents (typically £99) and the option of choosing an additional voluntary excess (up to £900). So if you had an overall £999 contents excess, for example, then you’d only be able to claim for accidental damage incidents which exceeded £999 in value.

Basic buildings accidental damage

- Customer slipped whilst getting into the bath has cracked the tub

- Customer returned from holiday to find the window on patio door at the rear of property was smashed as a result of being struck by a pigeon

Full buildings accidental damage

- Sewage pipe has collapsed. Part of the driveway needs to be dug up in order to access and replace the collapsed pipe

- Customer knocked radiator off the wall, damaging both radiator and wall

Basic contents accidental damage

- Customer went into the lounge to collect his phone charger and managed to swing the plug end into the TV which has cracked the screen.

- Customer was moving things around and dropped his Xbox down the stairs, resulting in it no longer working

Full contents accidental damage

- Customer has dropped her mobile phone on the kitchen floor, shattering it

- Customer tripped on the living room rug, whilst carrying a tin of paint. Paint damage to the rug, sofa, carpet and TV

Malicious damage is damage caused on purpose to the property of another person. This is different to accidental damage. Malicious damage is covered as standard under both buildings and contents cover (as long as it’s not caused by the property occupants or invited guests).

You can find a summary of what’s covered for both accidental damage for buildings and accidental damage for contents on this page.

For specifics, review the Policy Booklet. Buildings accidental damage is covered under section 1a and 1b, whilst contents accidental damage is covered under section 2b and 2c.

You can read about both accidental damage for buildings and accidental damage for contents on this page.

Please see our definition of accidental damage at the top of this page.

You might also be interested in…

Recommended by our customers

72% Saved money when they switched to Homeprotect*

*Survey data of 1,089 buying customers from 30th October – 12th November 2024

Prefer to SPEAK WITH us?

Our insurance experts are on hand if you have any questions.